Webinar examined SAF tax credits

Written by Jonathan Eisenthal

Two biofuel tax credits passed as part of the 2022 Inflation Reduction Act, 40B and 45Z, are key to boosting America’s nascent sustainable aviation fuel (SAF) sector. But the recently published guidance upon which 40B is based—and upon which 45Z could rely—needs improvement to ensure that corn-based ethanol can play a role in reducing aviation-related greenhouse gas emissions.

Those were among the key messages highlighted during “Clean Fuel Tax Credits,” a webinar covering 40B and 45Z hosted last month by the Minnesota Farmers Union, the Minnesota Biofuels Association, ,the Minnesota Corn Growers Association (MCGA), and the Minnesota Soybean Growers Association. Presenters included MCGA Senior Public Policy Director Amanda Bilek, Minnesota Farmers Union Climate and Working Lands Program Director Ariel Kagan, Minnesota Soybean Growers Association Executive Director Joe Smentek, and Minnesota Biofuels Association Executive Director Brian Werner.

Available in 2023 and 2024, 40B provides a tax credit to SAF that reduces lifecycle greenhouse gas (GHG) emissions by at least 50% compared to petroleum-based jet fuel. Meanwhile, 45Z will provide a tax credit in 2025, 2026, and 2027 to clean fuels, including SAF with a carbon intensity score below 50 kilograms of carbon dioxide equivalent per million British thermal units. The credits will go to the producers and blenders of the fuel.

The guidance released in April dictates how the U.S. Department of the Treasury will measure lifecycle GHG emissions for 40B and could serve as the base for the yet-to-be released 45Z guidance.

[More: Minnesota Corn will work to shape 45Z guidance]

During the webinar, speakers said they were pleased that the Treasury Department is using the Argonne Greenhouse gases, Regulated Emissions, and Energy use in Transportation (GREET) model for 40B. Developed by scientists at the Department of Energy Argonne National Laboratory, GREET is the gold standard for evaluating lifecycle emissions of various transportation fuels on a level playing field.

Speakers also said they are pleased that the updated GREET model for the first time incorporates the lifecycle emissions reductions provided by climate smart farming practices. But they urged the Treasury Department to have more nuance in accounting for the emissions reductions provided by these practices.

For example, Bilek urged the department to unbundle the use of no-till, cover crops, and enhance efficiency fertilizers and provide less burdensome tracking and verification processes. From the ethanol plant perspective, the Minnesota Biofuels Association’s Brian Werner also urged the department to broaden the number of practices and technologies that ethanol plants can get recognized for on their way to lowering their carbon intensity scores. For instance, plants can get credit for wind-generated electricity but not solar-generated electricity. They can utilize renewable natural gas but not gas created through anaerobic digestion.

Speakers during the webinar also noted how the short timeline built into the credits could be challenging, especially in Minnesota, where obtaining the air permits is a slow, cumbersome process. A recent Minnesota Chamber of Commerce study found that obtaining an air permit in Minnesota takes 1.5 to six times longer than other similarly sized states. Read more about the study here.

About 40B and 45Z

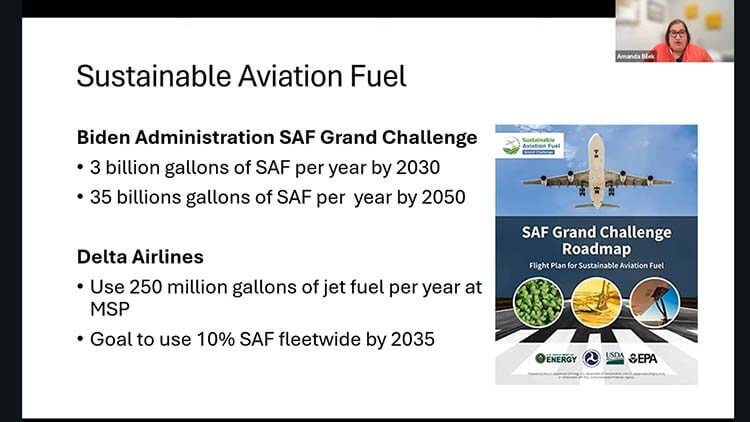

40B and 45Z offer a tax credit of up to $1.75 per gallon for aviation fuels made from renewable sources, depending upon the extent to which they reduce lifecycle GHG emissions. The tax credits serve as the first building blocks of the Sustainable Aviation Fuel Grand Challenge, which envisions reaching 3 billion gallons of SAF consumption by 2030 and 35 billion gallons by 2050. Such goals make clear the massive potential market for any feedstocks needed to blend SAF.

Delta Airlines, which utilizes the Minneapolis-St. Paul Airport as one of its hubs, has set a goal to use SAF for 10 percent of its fuel consumption by the end of the decade. That would be 25 million gallons of SAF jet fuel in Minnesota.

Alcohol-to-jet fuel, which can include the use of ethanol blended with kerosene jet fuel, is one of three recognized means to create SAF under 40B and 45Z. A second SAF pathway is known as hydro-processed esters and fatty acids and could make use of corn or soybean oil as a feedstock. A third method involves using renewable gas generated from wood waste or landfills.